New data on the e-levy in Ghana: unpopular tax on mobile money transfers is hitting the poor hardest

A lot of African countries have implemented taxes on electronic transactions Wikimedia Commons

Ghana’s introduction of a a 1.5% tax on mobile money transactions in May 2022 has been watched closely by policymakers across Africa. The proponents of the electronic transaction levy (e-levy) argue that taxes on mobile money — commonly referred to in Ghana as MoMo — present an opportunity for cash-strapped governments to raise funds in the complex post-pandemic context.

In Ghana, the “e-levy” has been linked to the current administration’s “Ghana Beyond Aid” strategy for reducing aid dependence.

Taxes on MoMo, in Ghana and elsewhere, have also been justified as a way to “capture” those working in the informal economy, who are perceived as being untaxed. Critics have pointed out, however, that informal workers (who make up 89% of total employment in Ghana) already pay a range of fees and taxes. Therefore they may be disproportionately affected by this new tax.

Despite much speculation about the impact of the e-levy, there has been little empirical evidence. In particular, it is important to consider how informal workers actually use mobile money, how the levy affects them and how they perceive it.

Our recent study looked at the likely impact of the levy on high and low earners in the informal economy. It was based on a representative survey of 2,700 informal sector operators – employers and own-account workers – in Accra before the tax was introduced. We found that despite the minimum threshold shielding some users, the tax likely has a negative impact on equity. We also found that informal workers’ scepticism about the tax was rooted in concerns about equity and in mistrust of the government more widely.

Assumption 1: e-levy will target higher earners

One of the assumptions prior to the implementation of the e-levy was that it would be an efficient way to target higher earning segments of the informal sector. These segments are perceived as being under-taxed and more likely than lower-income earners to use mobile money.

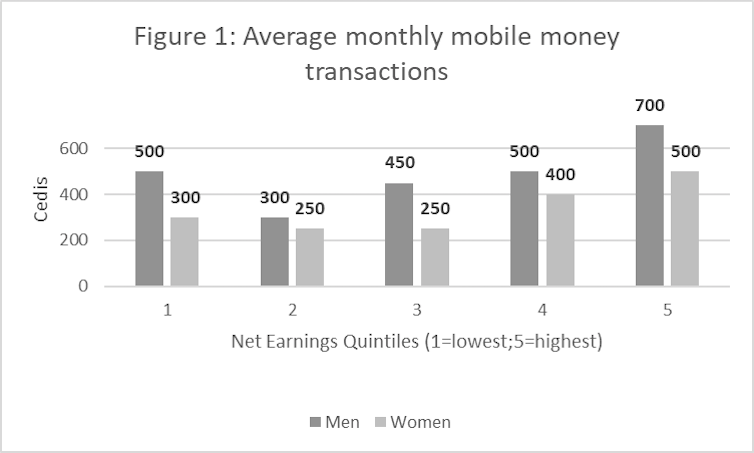

A key question, therefore, is whether mobile money usage is concentrated among higher income earners. This assumption only partially stands up to the evidence. We found that about half (51%) of the informal sector operators in Accra use mobile money. It is widely used by women and men, by different occupational groups and across the earnings distribution. But the distribution of the actual monthly transaction amounts is revealing (Figure 1).

Figure 1.

As expected, the top-earning group (quintile 5) reported transacting the most on the MoMo platform (about 500 and 700 cedis for female and male workers, respectively). However, lower-income earners will also be affected by the e-levy. This is because informal workers in the lowest earning group transacted more than those in several of the higher earnings categories.

About 41% of MoMo users in the informal sector do not have a bank account. Mobile money transfers may be particularly important for the unbanked, who typically account for the lower earning and more vulnerable segments of the workforce. We found 43% in the lowest earning quintile had bank accounts compared with 54% in the highest earning quintile.

Assumption 2: excluding small transactions will make the levy fair

It was anticipated that the exemption for transactions below 100 cedis per day would shield lower-income earners. It was expected to limit the negative impacts of the tax on the poor.

Based on MoMo usage data, we were able to estimate e-levy liability according to whether mobile money transactions in the previous month exceeded the 100 cedis threshold. Sixty-one percent of the users reported that they would be liable for some amount of e-levy payment based on their past MoMo transaction patterns and amounts. Here, our results provide some support for the government’s suggestion that the threshold would protect about 40% of MoMo users from taxation.

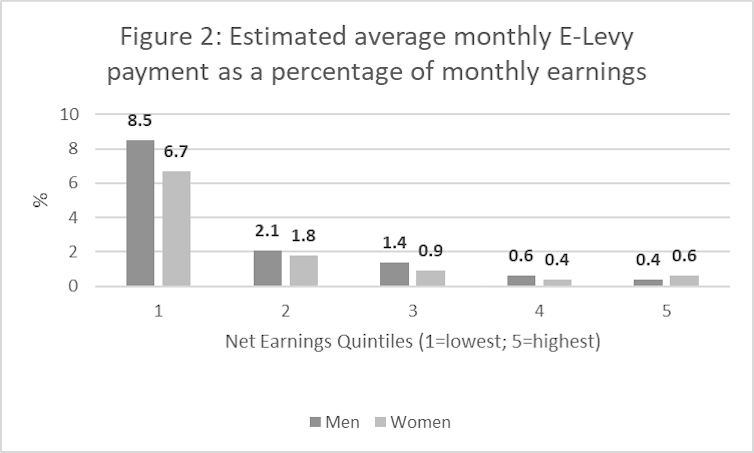

However, when the mobile money transaction amounts over the threshold are calculated as a share of earnings, it is clear that the levy is still a highly regressive tax (Figure 2) – meaning the tax burden is highest on the lowest earners.

Figure 2.

Lower earners bear a disproportionate share of the levy. The tax would account for just over 8% and 6% of monthly earnings for men and women, respectively, in the lowest earning quintile. Among the top earning quintile, in contrast, the projected tax would be less than 1% of earnings for both women and men.

Assumption 3: support for the e-levy would vary on political lines

As other surveys have highlighted, the e-levy is highly unpopular in Ghana. We found that 83% of Accra’s informal workers disapproved of it. They worried about how it would affect the poor, that it would be unfair, or raise an already high tax burden.

The levy was the subject of verbal and even physical fights in parliament between the two main parties. The New Patriotic Party administration blamed public opposition to the levy on alleged propaganda by the minority National Democratic Council. This might suggest that support for the levy would broadly fall along party lines. Our study found that supporters of the New Patriotic Party were indeed more likely to support the levy. But only 32% of them approved. Overall, perceptions of the government and its performance influenced opinions on the levy.

We also found that women were more critical of the e-levy, even when we controlled for a range of demographic and political features. Only 12% of women approved of it, compared with 21% of men. This striking difference highlights the importance of further research in this area, particularly to explore the relative impacts on men and women.

Implications for policy

The designers of Ghana’s e-levy argued that it would lead to a better distribution of the tax burden by bringing ostensibly untaxed informal sector workers into the tax net (fairness) while shielding the poorest (equity). While the threshold is successful in shielding some lower income users, we found, the e-levy is still highly regressive.

Our evidence suggests that the threshold should be raised and regularly adjusted for inflation. More generally, revenue authorities should focus on other ways of taxing high income workers in the informal economy, including professionals. At the very least, revenues from the e-levy should be used in a way that offsets its distributional impacts. This could mean targeting new spending on public infrastructure, goods and services that benefit informal workers. Government could also subsidise premiums paid by informal sector workers to join the National Health Insurance Scheme or contributions to the National Pension Scheme.

Our data suggests that key decisions about policy design and implementation were founded on assumptions that are not backed by empirical evidence. Continued research on the impacts of the e-levy in the coming months and years will help ensure that policymaking is evidence-based, with a more complete understanding of how the levy affects citizens and workers.

![]()

Mike Rogan a Research Associate with the Urban Policies Programme in WIEGO (Women in Informal Employment: Globalizing and Organizing). The research described in this article was made possible by generous support from the Swedish International Development Cooperation Agency.

Max Gallien is a research fellow at the Institute of Development Studies (IDS) and the International Centre for Tax and Development (ICTD). Through the ICTD, the research described in this article has also been supported by the UK Foreign, Commonwealth and Development Office, the Norwegian Agency for Development Cooperation and the Bill & Melinda Gates Foundation.

Vanessa van den Boogaard is a Research Fellow at the International Centre for Tax and Development (ICTD) and the University of Toronto.

Nana Akua Anyidoho does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.